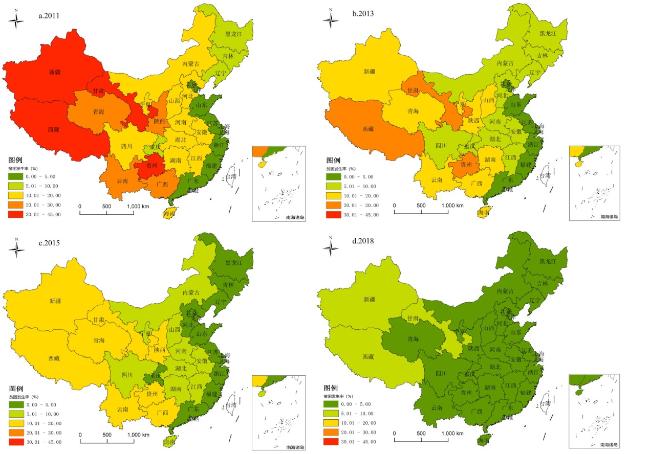

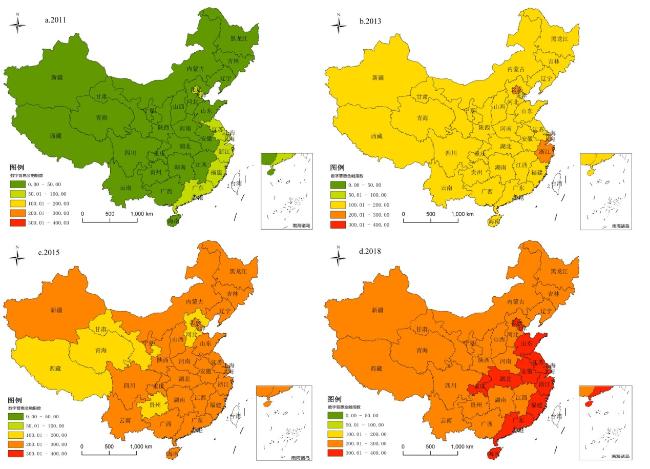

数字普惠金融的增收减贫效应——基于省际面板数据的实证分析

|

陈慧卿(1989—),男,湖南怀化人,硕士,讲师,研究方向为区域发展与农村经济。E-mail:273544680@qq.com |

收稿日期: 2020-08-26

修回日期: 2021-01-24

网络出版日期: 2025-04-30

基金资助

湖南省自然科学基金青年项目(2019JJ50112)

湖南省教育厅科学研究重点项目(19A120)

贵州省理论创新联合课题(GZLCLH-2019-007)

贵州财经大学引进人才科研启动项目(2018YJ57)

湖南省大学生创新训练项目(湘教通〔2020〕131号)

湖南工学院“双一流”建设重大培育项目(201709)

Effect of Digital Inclusive Finance on Increasing Rural Income and Reducing Poverty:Empirical Analysis Based on Inter-Provincial Panel Data

Received date: 2020-08-26

Revised date: 2021-01-24

Online published: 2025-04-30

陈慧卿 , 陈国生 , 魏晓博 , 彭六妍 , 张星星 . 数字普惠金融的增收减贫效应——基于省际面板数据的实证分析[J]. 经济地理, 2021 , 41(3) : 184 -191 . DOI: 10.15957/j.cnki.jjdl.2021.03.019

Digital inclusive finance plays a significant and positive role in poverty reduction. This article uses inter-provincial panel data from 2011 to 2018 to empirically analyze of the effect of digital inclusive finance on increasing rural income and poverty reduction. The results show that: 1) Digital inclusive finance has a significant poverty reduction effect,and the result is still valid in consideration of the endogenity. 2) The threshold effect model shows that the poverty reduction effect of digital inclusive finance will decrease with the increase of economic development level and the proportion of fiscal expenditure,and increase the urbanization level. 3) Research on regional heterogeneity shows that digital inclusive finance in the central region has the greatest effect on increasing rural incomes,followed by the east,and the smallest is the west,but the difference is not obvious. At the same time,the marginal contribution of digital inclusive finance to the poverty reduction effect of rural areas in the central and western regions is much higher than that of the eastern regions. The article proposes policy recommendations: improving the digital technology infrastructure (especially accelerating the construction of digital villages),promoting economic growth,improving the fiscal expenditure structure,and increasing the level of urbanization,improving the financial literacy of low-income groups,and strengthening the digital inclusive financial supervision system.

表1 不同区域的数字普惠金融增收减贫效应Tab.1 The effect of increasing income and reducing poverty of digital inclusive finance in different regions |

| I | IOP | ||||||

|---|---|---|---|---|---|---|---|

| 东部 | 中部 | 西部 | 东部 | 中部 | 西部 | ||

| FI | 0.0028***(12.74) | 0.0033***(7.30) | 0.0022***(8.97) | -0.0169***(-7.05) | -0.0639***(-7.36) | -0.0694***(-7.92) | |

| 控制变量 | 是 | 是 | 是 | 是 | 是 | 是 | |

| Sargan | 0.4261 | 0.2019 | 0.2526 | 0.2875 | 0.6456 | 0.7955 | |

| Hansen J | 0.4739 | 0.1336 | 0.2680 | 0.1824 | 0.5492 | 0.7561 | |

注:空号内为Z值,*、**、***分别代表在10%、5%、1%水平上显著。Hansen J和Sargan的输出结果为相应检验的p值。 |

表1 面板回归结果Tab.1 Panel regression results |

| 农村地区 收入增长(I) | 贫困程度(IOP) | ||||

|---|---|---|---|---|---|

| 模型(1) | 模型(2) | 模型(3) | 模型(4) | ||

| 数字普惠金融水平(FI) | 0.0029***(80.99) | 0.0020***(20.53) | -0.0480***(-18.61) | -0.0343***(-7.10) | |

| 经济发展水平(GDP) | 0.1370***(5.33) | -3.6502***(-3.76) | |||

| 第一产业结构(PI) | 0.4238*(1.85) | -53.1458***(-3.85) | |||

| 第二产业结构(SI) | 0.1398(1.48) | -25.1095***(-4.08) | |||

| 城镇化水平(UR) | 1.6860***(11.5) | -56.8942***(-7.60) | |||

| 财政支出比重(FE) | 0.4908***(4.82) | -15.6944***(-3.39) | |||

| 常数项 | 8.5031***(250.14) | 6.3116***(22.47) | 21.1699***(20.24) | 102.6244***(7.74) | |

| 控制区域 | 是 | 是 | 是 | 是 | |

| R2 | 0.8442 | 0.8977 | 0.6560 | 0.7788 | |

注:空号内为Z值,*、**、***分别代表在10%、5%、1%水平上显著。 |

表2 基于异方差估计方法的回归结果Tab.2 Regression results based on heteroscedasticity estimation method |

| 农村地区收入 增长(I)模型(5) | 贫困程度 (IOP)模型(6) | ||||

|---|---|---|---|---|---|

| 系数 | Z值 | 系数 | Z值 | ||

| 数字普惠金融水平(FI) | 0.0022*** | 14.37 | -0.0448*** | -11.06 | |

| 经济发展水平(GDP) | 0.1480*** | 9.13 | -2.0155*** | -4.64 | |

| 第一产业结构(PI) | 0.6270** | 2.00 | -35.8258*** | -4.27 | |

| 第二产业结构(SI) | 0.1619 | 1.07 | -22.1239*** | -5.48 | |

| 城镇化水平(UR) | 1.9620*** | 13.33 | -37.3448*** | -9.47 | |

| 财政支出比重(FE) | 0.6521*** | 7.15 | -5.4702** | -2.24 | |

| 常数项 | 5.9962*** | 21.50 | 71.3023*** | 9.55 | |

| 控制区域 | 是 | 是 | |||

| Sargan | 0.6538 | 0.4418 | |||

| Hansen J | 0.6795 | 0.3914 | |||

注:*、**、***分别代表在10%、5%、1%水平上显著;Sargan和Hansen J的输出结果为相应检验的p值。 |

表3 门槛效应检验结果及门槛变量估计值Tab.3 Threshold effect test results and Threshold variable estimates |

| 门槛变量 | 模型 | F值 | 临界值 | 门槛值 | 估计值 | ||

|---|---|---|---|---|---|---|---|

| 10% | 5% | 1% | |||||

| 经济发展水平(GDP) | 单一门槛 | 86.60*** | 40.8777 | 53.9830 | 80.6011 | 第一门槛值 | 7.3450 |

| 双重门槛 | 73.76*** | 35.4829 | 41.5866 | 62.6421 | 第二门槛值 | 9.9942 | |

| 三重门槛 | 23.23 | 59.5297 | 68.7996 | 102.7924 | |||

| 城镇化水平(UR) | 单一门槛 | 94.94** | 51.3915 | 75.3741 | 109.0859 | 第一门槛值 | 0.3110 |

| 双重门槛 | 101.51*** | 35.6877 | 42.9149 | 72.5720 | 第二门槛值 | 0.6271 | |

| 三重门槛 | 41.20 | 69.4461 | 82.9979 | 100.0609 | |||

| 财政支出比重(FE) | 单一门槛 | 136.56*** | 39.8370 | 52.4094 | 94.1258 | 第一门槛值 | 0.2681 |

| 双重门槛 | 69.84*** | 31.0803 | 36.8213 | 56.8270 | 第二门槛值 | 0.4288 | |

| 三重门槛 | 31.24 | 60.3459 | 76.0352 | 124.5931 | |||

注:*、**、***分别代表在10%、5%、1%水平上显著,Bootsrap次数为500次。 |

表4 面板门槛模型回归结果(因变量为贫困程度)Tab.4 Panel threshold model regression results (dependent variable is poverty level) |

| 解释变量(FI) | GDP门槛模型 | UR门槛模型 | FE门槛模型 |

|---|---|---|---|

| GDP≤7.3450 | -0.1031*** (-8.56) | ||

| 7.3450<GDP≤9.9942 | -0.0621*** (-21.7) | ||

| 9.9942<GDP | -0.0365*** (-14.41) | ||

| UR≤0.3110 | -0.0268*** (-8.41) | ||

| 0.3110<UR≤0.6271 | -0.0577*** (-23.12) | ||

| 0.6271<UR | -0.1005*** (-8.47) | ||

| FE≤0.2681 | -0.1046*** (-21.78) | ||

| 0.2681<FE≤0.4288 | -0.0585*** (-20.37) | ||

| 0.4288<FE | -0.0333*** (-15.41) | ||

| 常数项 | 17.1875*** (37.93) | 16.8239*** (38.05) | 15.7967*** (41.57) |

| R2 | 0.7226 | 0.7294 | 0.8030 |

| F值 | 25.22*** | 25.10*** | 35.72*** |

注:空号内为T值,*、**、***分别代表在10%、5%、1%水平上显著。 |

| [1] |

尹应凯, 侯蕤. 数字普惠金融的发展逻辑、国际经验与中国贡献[J]. 学术探索, 2017(3):104-111.

|

| [2] |

刘长庚, 罗午阳. 互联网使用与农户金融排斥——基于CHFS2013的实证研究[J]. 经济经纬, 2019, 36(2):141-148.

|

| [3] |

刘锦怡, 刘纯阳. 数字普惠金融的农村减贫效应:效果与机制[J]. 财经论丛, 2020(1):43-53.

|

| [4] |

王刚贞, 谢露露. 数字普惠金融减贫效应的作用机理与实证检验——基于中国省际面板数据的分析[J]. 安徽农业大学学报:社会科学版, 2020, 29(1):1-10.

|

| [5] |

张勋, 万广华, 张佳佳, 等. 数字经济、普惠金融与包容性增长[J]. 经济研究, 2019, 54(8):71-86.

|

| [6] |

黄倩, 李政, 熊德平. 数字普惠金融的减贫效应及其传导机制[J]. 改革, 2019(11):90-101.

|

| [7] |

|

| [8] |

|

| [9] |

|

| [10] |

钱鹏岁, 孙姝. 数字普惠金融发展与贫困减缓——基于空间杜宾模型的实证研究[J]. 武汉金融, 2019(6):39-46.

|

| [11] |

武丽娟, 徐璋勇. 我国农村普惠金融的减贫增收效应研究——基于4023户农户微观数据的断点回归[J]. 南方经济, 2018(5):104-127.

|

| [12] |

赵丙奇, 李露丹. 中西部地区20省份普惠金融对精准扶贫的效果评价[J]. 农业经济问题, 2020(1):104-113.

|

| [13] |

杨俊, 王燕, 张宗益. 中国金融发展与贫困减少的经验分析[J]. 世界经济, 2008(8):62-76.

|

| [14] |

|

| [15] |

向晖, 郭珍珍. 金融素养对网贷消费行为的影响——感知风险中介作用的实证研究[J]. 消费经济, 2019, 35(2):62-70.

|

| [16] |

王伟, 朱一鸣. 普惠金融与县域资金外流:减贫还是致贫——基于中国592个国家级贫困县的研究[J]. 经济理论与经济管理, 2018(1):98-108.

|

| [17] |

邱兆祥, 向晓建. 数字普惠金融发展中所面临的问题及对策研究[J]. 金融理论与实践, 2018(1):5-9.

|

| [18] |

|

| [19] |

黄秋萍, 胡宗义, 刘亦文. 中国普惠金融发展水平及其贫困减缓效应[J]. 金融经济学研究, 2017, 32(6):75-84.

|

| [20] |

龚沁宜, 成学真. 数字普惠金融、农村贫困与经济增长[J]. 甘肃社会科学, 2018(6):139-145.

|

| [21] |

崔艳娟, 孙刚. 金融发展是贫困减缓的原因吗?——来自中国的证据[J]. 金融研究, 2012(11):116-127.

|

| [22] |

张兵, 翁辰. 农村金融发展的减贫效应——空间溢出和门槛特征[J]. 农业技术经济, 2015(9):37-47.

|

| [23] |

师荣蓉, 徐璋勇, 赵彦嘉. 金融减贫的门槛效应及其实证检验——基于中国西部省际面板数据的研究[J]. 中国软科学, 2013(3):32-41.

|

| [24] |

王爱萍, 胡海峰, 张昭. 金融发展对收入贫困的影响及作用机制再检验——基于中介效应模型的实证研究[J]. 农业技术经济, 2020(3):70-83.

|

| [25] |

李建军, 卢盼盼. 中国居民金融服务包容性测度与空间差异[J]. 经济地理, 2016, 36(3):118-124.

|

| [26] |

程惠霞, 杨璐. 中国新型农村金融机构空间分布与扩散特征[J]. 经济地理, 2020, 40(2):163-170.

|

| [27] |

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}