县域数字普惠金融发展的空间格局演化与影响因素分析——以湖南省为例

|

李明贤(1968—),女,陕西大荔人,博士,教授,博士生导师,研究方向为农村金融。E-mail:limingxian6856@hunau.edu.cn |

收稿日期: 2020-08-24

修回日期: 2021-04-20

网络出版日期: 2025-04-13

基金资助

国家自然科学基金项目(72073043)

湖南省教育厅重点科研项目(19A230)

湖南省研究生科研创新项目(CX20200666)

Development Level of County Digital Inclusive Finance: Spatial Pattern Evolution and Influencing Factors Analysis:Take Hunan Province as an Example

Received date: 2020-08-24

Revised date: 2021-04-20

Online published: 2025-04-13

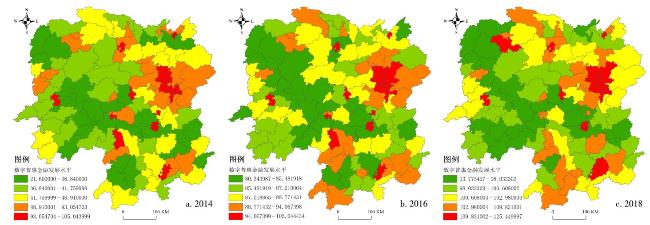

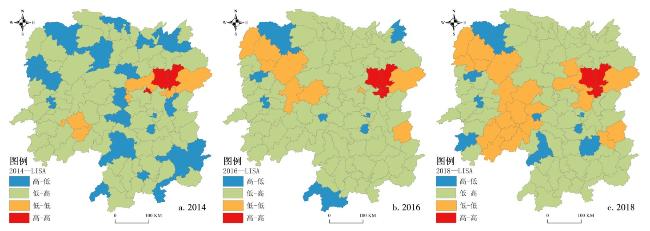

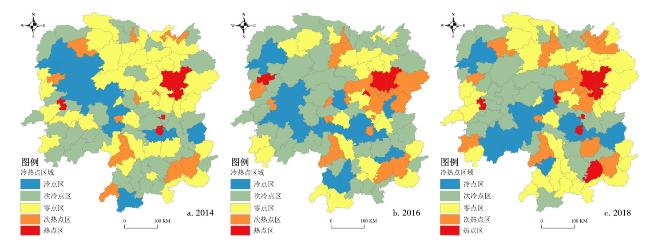

县域是普惠金融发展的主战场,发展县域数字普惠金融是统筹城乡发展的重要手段。文章通过研究湖南省县域数字普惠金融发展的空间分异性与相关性,揭示县域数字普惠金融发展的空间分异格局及演化过程,并利用面板数据模型考察其主要影响因素。研究发现:①湖南省县域数字普惠金融发展呈现出较为明显的区域差异,这种差异存在“固化”特征;②数字普惠金融发展按主要板块呈现集聚特征;③不同区域内县域数字普惠金融发展的主要影响因素存在异质性;④传统金融发展水平和经济发展水平对湖南省内不同区域的县域数字普惠金融发展均有促进作用,政府干预程度在传统金融发展水平与数字普惠之间起调节作用,会抑制传统金融发展对县域数字普惠金融的促进作用。据此,文章提出推动县域数字普惠金融高质量发展的相关对策建议。

李明贤 , 郑洲舟 , 陈铯 . 县域数字普惠金融发展的空间格局演化与影响因素分析——以湖南省为例[J]. 经济地理, 2021 , 41(8) : 136 -143 . DOI: 10.15957/j.cnki.jjdl.2021.08.016

County is the important part of the development of inclusive finance,and the development of county's digital inclusive finance is an important means for coordinating urban and rural development. By studying the spatial pattern and correlation of the development of digital inclusive finance in counties of Hunan Province,this paper reveals its spatial differentiation pattern and evolution process,and investigates its main influencing factors applying the panel data model. It reveals that: 1) The development of digital inclusive finance in counties of Hunan Province presents obvious regional differences,which have the characteristic of "solidification". 2) It presents agglomeration characteristic in different main sectors. 3) The main factors affecting the development of digital inclusive finance are heterogeneous in different regions. 4) The traditional financial development level and economic development level both can promote the development of digital inclusive finance in counties of Hunan Province,and the degree of government intervention plays a enhancing role in the development of digital inclusive finance in counties of Hunan Province,which will inhibit the promotion of traditional financial development to county's digital inclusive finance. Accordingly,it puts forward relevant countermeasures and suggestions to promote the high-quality development of county's digital inclusive finance.

表1 湖南省县域数字普惠金融的Moran's I系数Tab.1 The Moran's I coefficient of digital inclusive finance in counties of Hunan Province |

| 年份 | Moran's I | Z | P | E(I) | Var(I) |

|---|---|---|---|---|---|

| 2014 | 0.3064 | 4.4791 | 0.0010 | -0.0100 | 0.0054 |

| 2015 | 0.2464 | 4.3822 | 0.0010 | -0.0100 | 0.0035 |

| 2016 | 0.2807 | 4.1427 | 0.0010 | -0.0100 | 0.0049 |

| 2017 | 0.2305 | 3.9487 | 0.0010 | -0.0100 | 0.0038 |

| 2018 | 0.3041 | 4.4419 | 0.0010 | -0.0100 | 0.0050 |

表2 变量说明Tab.2 Variable explanation |

| 主要因素 | 变量名称 | 测度方法 | 符号预期 |

|---|---|---|---|

| 数字普惠金融发展水平因素 | 县域数字普惠金融水平 | 来自北京大学数字普惠金融指数(2011—2018) | |

| 经济因素 | 传统金融发展程度 | 金融相关比(存贷款总额与GDP总额的比值) | + |

| 经济发展水平 | 人均GDP作为代理变量 | + | |

| 第三产业发展水平 | 第三产业产值/GDP | + | |

| 城镇化水平 | 非农人口比重(二、三产业从业人口)/户籍人口) | + | |

| 社会因素 | 政府干预程度 | 公共财政支出/GDP | |

| 互联网发展水平 | 智能手机普及率(每百人智能手机数) | - | |

| 人口特征因素 | 人口受教育水平 | 中小学在校学生数/年末常住人口 | + |

| 收入水平 | 人均可支配收入 | + |

表3 基准线性回归分析Tab.3 The baseline regression |

| 全样本(1) | 大湘南板块(2) | 大湘西板块(3) | 洞庭湖板块(4) | 长株潭板块(5) | |

|---|---|---|---|---|---|

| 传统金融发展程度 | 22.7200***(5.10) | 20.5600**(2.25) | 21.3100***(2.89) | 29.0300***(2.84) | 37.5700***(3.26) |

| 经济发展水平 | 0.0003***(3.77) | 0.0006***(2.99) | 0.0002*(1.76) | 0.0011***(3.04) | 0.0004**(2.68) |

| 第三产业发展水平 | 71.0900***(5.17) | 102.6000***(3.45) | 49.3200**(2.31) | 23.2500(0.82) | 77.4200(1.67) |

| 城镇化水平 | -0.0042**(-2.48) | -0.0059*(-1.92) | -0.0033(-1.15) | -0.0009(-0.23) | -0.0033(-0.77) |

| 政府干预程度 | -10.3400(-0.62) | -0.1280(-0.00) | -18.8100(-0.71) | 15.5400(0.41) | -87.7000*(-1.86) |

| 互联网发展水平 | -0.0000**(-2.27) | -0.0001*(-1.82) | -0.0000(-0.62) | -0.0001**(-2.10) | -0.0001**(-2.15) |

| 人口受教育水平 | 0.0024(0.45) | 0.0066(0.71) | 0.0020***(3.19) | -0.0080(-0.64) | 0.0008(0.92) |

| 收入水平 | 0.0025***(6.34) | 0.0029***(3.82) | 0.0028(0.30) | 0.0022*(1.98) | -0.0029(-0.23) |

| 常数 | -8.5480(-1.02) | -31.8500**(-2.12) | 9.4710(0.71) | -7.9980(-0.36) | 22.5300(0.80) |

| N | 335 | 93 | 133 | 66 | 43 |

| R2 | 0.3880 | 0.5350 | 0.2980 | 0.3770 | 0.5520 |

注:t statistics in parentheses;*p<0.1;**p<0.05;***p<0.01。表4同。 |

表4 交互项回归Tab.4 Reciprocal regression |

| 全样本(1) | 大湘南板块(2) | 大湘西板块(3) | 洞庭湖板块(4) | 长株潭板块(5) | |

|---|---|---|---|---|---|

| 传统金融发展程度 | 22.8500***(5.16) | 20.8500**(2.28) | 21.2600***(2.90) | 37.1500***(3.65) | 37.3400***(3.17) |

| 政府干预程度 | 16.7300(0.82) | 17.2200(0.45) | 14.1500(0.42) | 90.0400*(1.98) | -81.4100(-1.35) |

| 传统金融发展程度×政府干预 | -42.8600**(-2.27) | -41.6700(-0.93) | -47.8600(-1.56) | -109.0000**(-2.66) | -7.9930(-0.17) |

| 其他控制变量 | Yes | Yes | Yes | Yes | Yes |

| N | 335 | 93 | 133 | 66 | 43 |

| R2 | 0.3980 | 0.5403 | 0.3113 | 0.4468 | 0.5526 |

| [1] |

陈文胜. 中国县域发展的基本特征与历史演进[J]. 中国发展观察, 2014(6):30-31.

|

| [2] |

唐宁. 数字普惠金融的中国实践与未来发展[J]. 清华金融评论, 2016, 37(12):49-50.

|

| [3] |

李明贤, 陈铯. 金融科技、授信方式改进与涉农金融机构普惠能力提升[J]. 经济体制改革, 2021(2):88-94.

|

| [4] |

|

| [5] |

|

| [6] |

|

| [7] |

|

| [8] |

陆凤芝, 黄永兴, 徐鹏. 中国普惠金融的省域差异及影响因素[J]. 金融经济学研究, 2017, 32(1):111-120.

|

| [9] |

李雅宁, 吴博文, 罗欣, 等. 我国三十一省区普惠金融发展现状分析[J]. 北方经贸, 2017(2):116-118.

|

| [10] |

贺大维. 数字普惠金融发展对中国城乡收入差距的影响研究[D]. 济南: 山东大学, 2019.

|

| [11] |

杜佳倩. 中国数字普惠金融发展评价及影响因素分析[D]. 武汉: 中南财经政法大学, 2019.

|

| [12] |

吴本健, 毛宁, 郭利华. “双重排斥”下互联网金融在农村地区的普惠效应[J]. 华南师范大学学报:社会科学版, 2017(1):94-100,190.

|

| [13] |

张正平, 张俊美. 发展农村数字普惠金融的路径[J]. 中国金融家, 2021(4):57-58,85.

|

| [14] |

刘传明, 王卉彤, 魏晓敏. 中国八大城市群互联网金融发展的区域差异分解及收敛性研究[J]. 数量经济技术经济研究, 2017, 34(8):3-20.

|

| [15] |

潘竟虎. 中国地级及以上城市城乡收入差距时空分异格局[J]. 经济地理, 2014, 34(6):60-67.

|

| [16] |

|

| [17] |

|

| [18] |

|

| [19] |

王宇熹, 范洁. 消费者金融素养影响因素研究——基于上海地区问卷调查数据的实证分析[J]. 金融理论与实践, 2015(3):70-75.

|

| [20] |

王立国, 赵婉妤. 我国金融发展与产业结构升级研究[J]. 财经问题研究, 2015(1):22-29.

|

| [21] |

蒋庆正, 李红, 刘香甜. 农村数字普惠金融发展水平测度及影响因素研究[J]. 金融经济学研究, 2019, 34(4):123-133.

|

| [22] |

张前程, 龚刚. 政府干预、金融深化与行业投资配置效率[J]. 经济学家, 2016(2):60-68.

|

| [23] |

吴娅玲, 潘林伟. 区域金融发展中地方政府干预的行为边界及影响[J]. 当代经济管理, 2016, 38(1):64-68.

|

| [24] |

周业安, 赵晓男. 地方政府竞争模式研究——构建地方政府间良性竞争秩序的理论和政策分析[J]. 管理世界, 2002(12):52-61.

|

| [25] |

林胜, 边鹏, 闫晗. 数字普惠金融政策框架国内外比较研究[J]. 征信, 2020, 38(1):78-82.

|

| [26] |

孟娜娜, 粟勤. 挤出效应还是鲶鱼效应:金融科技对传统普惠金融影响研究[J]. 现代财经, 2020(1):56-70.

|

| [27] |

邱兆祥, 向晓建. 数字普惠金融发展中所面临的问题及对策研究[J]. 金融理论与实践, 2018(1):5-9.

|

| [28] |

廖婧琳, 周利. 数字普惠金融、受教育水平与家庭风险金融资产投资[J]. 现代经济探讨, 2020(1):42-53.

|

| [29] |

易行健, 周利. 数字普惠金融发展是否显著影响了居民消费——来自中国家庭的微观证据[J]. 金融研究, 2018(11):47-67.

|

| [30] |

任碧云, 李柳颍. 数字普惠金融是否促进农村包容性增长——基于京津冀2114位农村居民调查数据的研究[J]. 现代财经(天津财经大学学报), 2019, 39(4):3-14.

|

| [31] |

北京大学数字金融研究中心课题组. 北京大学数字普惠金融指数(011-2018年)[R]. 北京: 北京大学数字金融研究中心, 2019.

|

| [32] |

郭峰, 王靖一, 王芳, 等. 测度中国数字普惠金融发展:指数编制与空间特征[J]. 经济学(季刊), 2020, 19(4):1401-1418.

|

| [33] |

|

| [34] |

|

| [35] |

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}