上市公司(总部)地理位置的分歧——兼论企业位置标准与区位理论发展创新

|

胡国建(1992—),男,讲师,硕士生导师,研究方向为经济地理与区域发展。E-mail:guojianhu1992@163.com |

收稿日期: 2023-04-12

修回日期: 2023-12-29

网络出版日期: 2024-06-03

基金资助

国家自然科学基金项目(42171171)

国家自然科学基金项目(42361050)

The Divergence of Geographical Location of Listed Companies (Headquarters): On the Standard of Enterprise Location and the Development of Location Theory

Received date: 2023-04-12

Revised date: 2023-12-29

Online published: 2024-06-03

胡国建 , 陆玉麒 , 钟业喜 . 上市公司(总部)地理位置的分歧——兼论企业位置标准与区位理论发展创新[J]. 经济地理, 2024 , 44(1) : 130 -138 . DOI: 10.15957/j.cnki.jjdl.2024.01.013

The "office address" and "registration address" of the listed company,which are the only two standards for judging the geographical location of the headquarters,are not spatially identical. This phenomenon may lead to inconsistencies between the location or regional attribution of listed companies (headquarters) defined in numerous literature and the reality,thereby questioning the credibility of research data and conclusions. Based on multidisciplinary literature,this article expounds the divergence of enterprise location and its impact on empirical research,verifies the ability of office address and registration address to represent the location of A-share listed companies (headquarters),and discusses the criteria of enterprise location under different circumstances and its impact on location theory. The results show that: 1) The separation of the office address and the registration address will inevitably lead to the discrepancy between the location and the region of the listed company (headquarters) defined in some literatures and the reality,and cause errors in enterprise indicators,regional indicator statistics and enterprise distance,which makes the credibility of the research conclusion doubtful. 2) Among the 117 A-share listed companies with cross-province separation of office address and registration address,up to 85.48% of the company headquarters and office address are the same,the office address is much better than the registration address in representing the location of the company (headquarters),so the relevant research of listed companies should take the office address as the location of the company (headquarters),and the existing literature using registration address should be re-examined. 3) In fact,the separation between business premises and registration address is quite common. The location of the company (headquarters) in economic geography is be a business premises that undertakes economic functions and occupies a certain geographical space,and the registration address should only be applied in a few non-economic research and data statistics. It should pay more attention to the separation of registration address and business premises,which will be beneficial to the development and innovation of location theory in the aspects of location subject,location phenomenon, location factor and location influence.

表1 办公地址和注册地址作为公司(总部)位置的依据Tab.1 Reasons for office address and registration address as the location of the company (headquarters) |

| 类别 | 文献题名 | 具体描述 |

|---|---|---|

| 办公地界定企业(总部)位置 | 我国A股市场地域联动性的实证研究[3] | “公司在选择注册地址时往往会考虑税收、政府优惠等因素,但公司的经营业务并不一定在注册地址开展。因此公司的办公地址作为公司与外界联系和业务交流的地方,更具有实际意义” |

| 上市公司地理位置、风险投资参与与股票流动性——基于创业板市场的实证研究[22] | “考虑到现实中存在公司的注册地址并非经营地的情况,本文在选取地理位置指标时采用上市公司的办公地址所在城市度量” | |

| The changing geography of domestic financial city network in China,1995-2015[9] | “由于少数企业的注册地不是实际运营总部所在地,本文选择实际办公地址作为总部所在地” | |

| 注册地界定企业(总部)位置 | 金融集团内的信息流动与基金投资业绩[7] | “考虑到办公地址的多变性,本文采用两者的注册地址作为两者的总部所在地” |

| 高铁开通与公司业绩:来自中国上市公司的经验证据》[8] | “一家上市公司的办公地址可能有很多位置,因此本文为简化研究复杂性选取了上市公司注册地址” | |

| Should Tax Policy Target Multinational Firm Headquarters[17] | “可以将公司在税务方面的合法住所(注册地址)视为衡量总部的标准” |

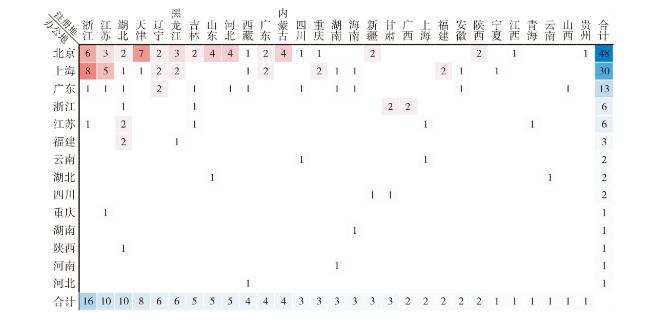

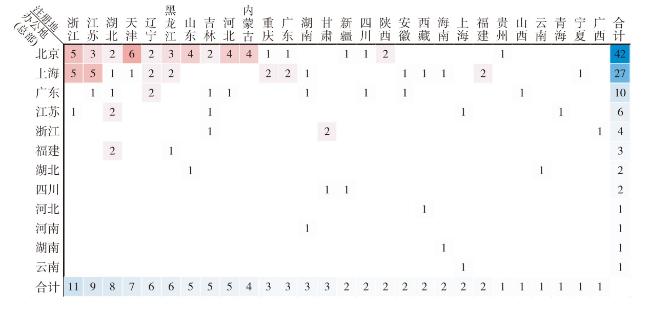

表2 总部位于注册地的16家上市公司Tab.2 16 listed companies headquartered in the registration province |

| 公司简称 | 注册地址 (总部) | 办公地址 | 公司简称 | 注册地址 (总部) | 办公地址 |

|---|---|---|---|---|---|

| 神州信息 | 广东 | 北京 | 光电股份 | 湖北 | 陕西 |

| 天音控股 | 江西 | 北京 | 森马服饰 | 浙江 | 上海 |

| 国机汽车 | 天津 | 北京 | 申通快递 | 浙江 | 上海 |

| 易明医药 | 西藏 | 北京 | 利欧股份 | 浙江 | 上海 |

| 中油工程 | 新疆 | 北京 | 易见股份 | 四川 | 云南 |

| 天马股份 | 浙江 | 北京 | 天夏智慧 | 广西 | 浙江 |

| 万兴科技 | 西藏 | 广东 | 闻泰科技 | 湖北 | 浙江 |

| 盈峰环境 | 浙江 | 广东 | 科林环保 | 江苏 | 重庆 |

表3 公司倒置的相关文献Tab.3 Related literature on corporate inversions |

| 文献 | 具体描述 |

|---|---|

| Home-country effects of corporate inversions[11] | “在对倒置计划的描述中,诺贝尔公司明确表示,注册地址的迁出不会影响诺贝尔的员工,所有的运营总部职能(包括研发)将留在瑞典,生产设施也不会受到影响”;“夏尔公司的注册地址倒置到爱尔兰的唯一结果是侵蚀了英国的税基,夏尔公司在英国的经济活动没有任何值得关注的整体变化,无论是积极的还是消极的。在企业战略层面上,(注册地址)搬迁似乎完全是虚拟的” |

| Corporate inversion:A symbol of a changing paradigm of corporate behavior[33] | “(公司倒置)在大多数情况下,公司的总部、业务和雇员的位置不会改变,在新的注册地几乎没有实体存在” |

| Do tax havens divert economic activity[34] | “有证据表明,公司倒置不会导致实体经济活动从非避税天堂管辖区转移出去” |

| Solving the corporate inversion phenomenon:An exercise in free market patriotism,protectionism through facilitation[35] | “倒置不涉及公司的实际搬迁,该交易更具象征意义,因为实质性的变化只反映在商业协议中。一般来说,公司的内部运作没有任何变化。美国公司倒置后,其管理和商业运作通常仍在美国,该公司只是放弃其美国公民身份” |

| Tax planning strategies for corporate inversion[36] | “更多的时候,(倒置的美国公司)在美国的业务根本没有改变,总部和管理团队仍然在美国” |

| [1] |

关皓明, 杨青山, 浩飞龙, 等. 基于“产业—企业—空间”的沈阳市经济韧性特征[J]. 地理学报, 2021, 76(2):415-427.

|

| [2] |

|

| [3] |

刘磊. 我国A股市场地域联动性的实证研究[D]. 大连: 东北财经大学, 2015.

|

| [4] |

|

| [5] |

蔡宏标, 饶品贵. 机构投资者、税收征管与企业避税[J]. 会计研究, 2015(10):59-65,97.

|

| [6] |

孙玉涛, 刘凤朝. 中国企业技术创新主体地位确立——情境、内涵和政策[J]. 科学学研究, 2016, 34(11):1716-1724.

|

| [7] |

曹洁. 金融集团内的信息流动与基金投资业绩[D]. 马鞍山: 安徽工业大学, 2012.

|

| [8] |

尹齐炜. 高铁开通与公司业绩:来自中国上市公司的经验证据[D]. 武汉: 中南财经政法大学, 2019.

|

| [9] |

|

| [10] |

谭劲松, 陈艳艳, 谭燕. 地方上市公司数量、经济影响力与企业长期借款——来自我国A股市场的经验数据[J]. 中国会计评论, 2010, 8(1):31-52.

|

| [11] |

|

| [12] |

邢丽, 郝晓婧. 全球最低企业税:意图、影响及政策选择[J]. 地方财政研究, 2021(12):103-112.

|

| [13] |

张可云, 裴相烨. 大城市制造业企业空间扩张模式及其对企业效率的影响——以北京市上市企业为例[J]. 地理科学进展, 2021, 40(10):1613-1625.

|

| [14] |

蒋子龙, 王军, 樊杰. 1990—2019年中国上市公司总部分布变迁及影响因素[J]. 经济地理, 2022, 42(4):112-121.

|

| [15] |

胡国建, 陆玉麒, 胡舒云. 顾及企业注册地址的区位理论研究[J]. 地理研究, 2022, 41(2):580-595.

|

| [16] |

毕茜, 顾立盟, 张济建. 传统文化、环境制度与企业环境信息披露[J]. 会计研究, 2015(3):12-19,94.

|

| [17] |

|

| [18] |

|

| [19] |

李玲. 高铁站区发展的影响因素研究——以京沪高铁站区为例[D]. 北京: 北京交通大学, 2019.

|

| [20] |

吴波, 郝云宏, 魏立春. 中国上市公司总部迁移的动向与动因研究[J]. 经济地理, 2012, 32(12):8-14.

|

| [21] |

|

| [22] |

|

| [23] |

白京羽, 林晓锋, 丁俊琦. 我国生物产业发展现状及政策建议[J]. 中国科学院院刊, 2020, 35(8):1053-1060.

|

| [24] |

蔡庆丰, 陈熠辉, 林焜. 信贷资源可得性与企业创新:激励还是抑制?——基于银行网点数据和金融地理结构的微观证据[J]. 经济研究, 2020, 55(10):124-140.

|

| [25] |

沈甜甜, 汪洋. 上市公司地理位置、风险投资参与与股票流动性——基于创业板市场的实证研究[J]. 金融理论与实践, 2020(8):85-95.

|

| [26] |

|

| [27] |

胡国建, 金星星, 陆玉麒, 等. 中国上市公司总部与注册地跨城市分离的格局、形成过程和影响因素[J]. 地理研究, 2021, 40(2):402-418.

|

| [28] |

朱超. 自贸区背景下宁波FT贸易公司发展战略研究[D]. 杭州: 浙江理工大学, 2017.

|

| [29] |

郭富青. 我国企业住所与经营场所分离与分制改革的法律探析[J]. 现代法学, 2020, 42(2):145-156.

|

| [30] |

汪雨卉. 多源大数据视角下上海市初创企业集聚演化特征研究[D]. 上海: 上海师范大学, 2019.

|

| [31] |

李孝猛. 公司住所登记审查的法律限度[J]. 上海政法学院学报(法治论丛), 2013, 28(2):107-116.

|

| [32] |

李小建, 李国平, 曾刚, 等. 经济地理学(第三版)[M]. 北京: 高等教育出版社, 2018.

|

| [33] |

|

| [34] |

|

| [35] |

|

| [36] |

|

| [37] |

郭婧婷, 陶书宁. 霍尔果斯“转折”[J]. 商讯, 2018(12):5-8.

|

| [38] |

|

| [39] |

李广隆. 科学防控公司登记注册地址风险探究[J]. 中国市场监管研究, 2018(2):72-74.

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}